Ethiopian Income Tax Calculator

by EthioLab

🗂️ Finance

Version 10.0.3 💾 1 Mb

📅 Updated June 26, 2020

Income tax calculator based on Ethiopian Labor Law

Features Ethiopian Income Tax Calculator

Taxes on monthly salaries are calculated during the monthly payroll preparation and have to be paid to tax authorities within one month after having been deducted from the employee.

The same applies also for the various provident funds and pension schemes.

There are stiff penalties for late submission of tax returns and all other statutory deductions.

The directives for fringe benefits and other income from employment are sometimes difficult to apply due to inefficient distribution of directives to all stakeholders.

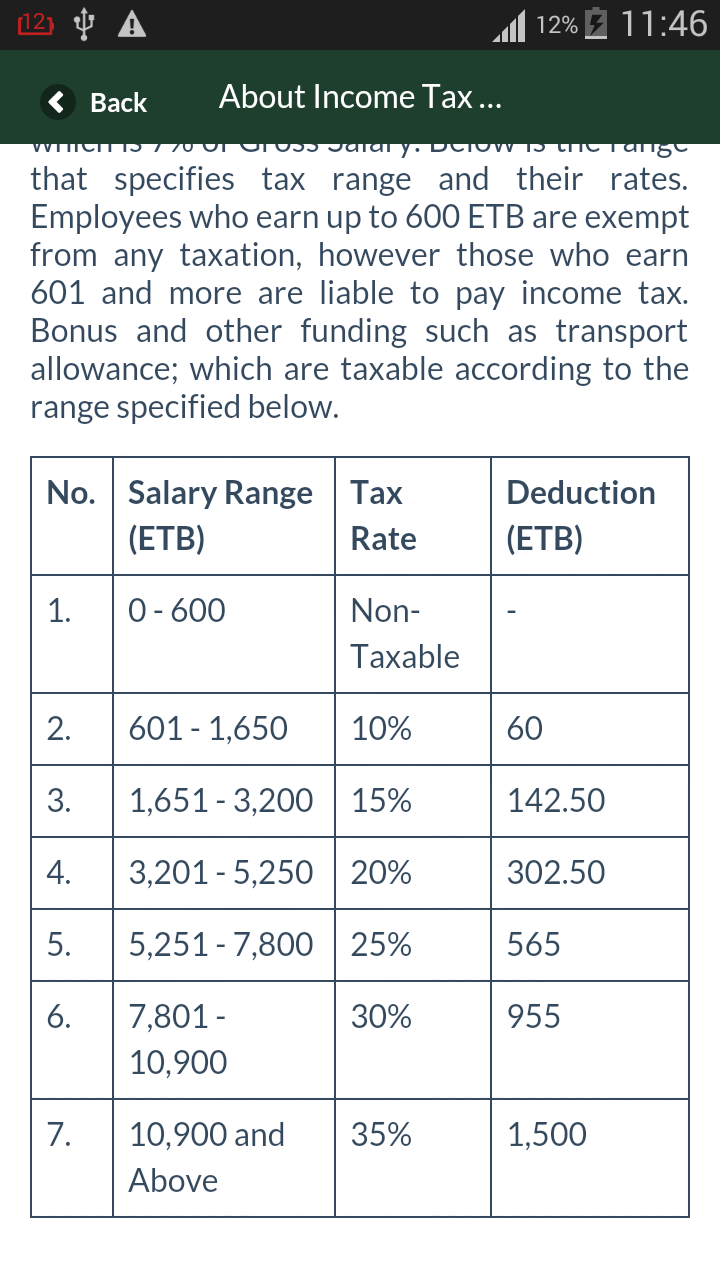

In Ethiopia, all income from employment like various allowances like fuel, representation, cash indemnities etc.

are taxable.

The tax rates for payout for accrued, unutilized annual leave during termination processing are heavy: they are pro-rated over the period of months the income applies to and are subject to the maximum tax rate.

The tax rate for severance pay, however, is much lighter as it is taxed at a monthly salary rate to support the concept that the employee may not have financial difficulties whilst searching for his next employment.

Employment contracts whether permanent or temporary are always copied to the private organization employees’ pension offices.

The rates applied for provident fund & pension schemes sometimes confuse accountants and cause inaccuracies as the rates for provident fund varies from company to company.

Payments for outstanding performance or the award of cash prizes at times like marriage are not tax effective.

They are taxed at the same rate as the normal monthly salaries.Most allowances like fuel, representation & house allowances are taxed fully as long as the whole remuneration package is above a certain level.

Weather Features

Get accurate weather forecasts and real-time updates.

Fitness Tracking

Track your workouts and monitor your health metrics.

Learning Tools

Enhance your learning experience with interactive features.

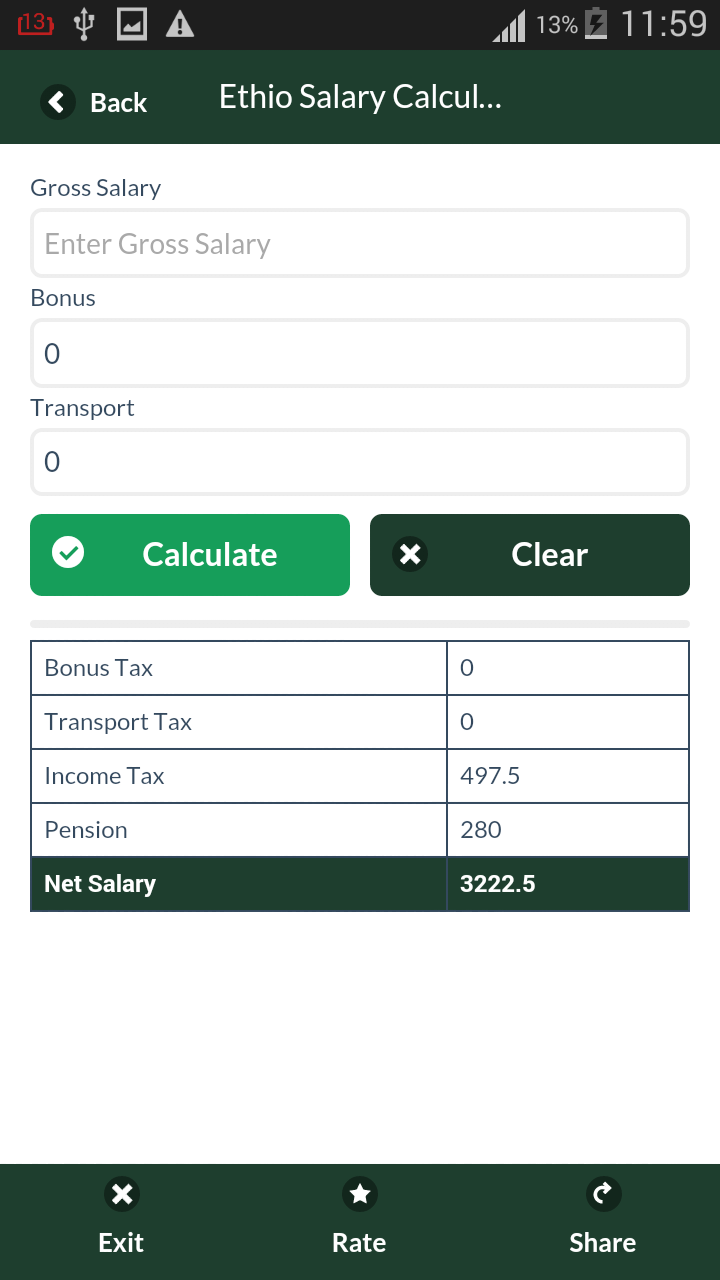

See the Ethiopian Income Tax Calculator in Action

What Our Users Say

Don't just take our word for it. Here's what our users have to say about our Android app.

"Incredible"

ከዚህም ከዚያም

"አመሰግናለሁ በጣም"

Rayane Haile

"all free"

BILATU TENKIR

"Ethioian income This is very cute and very nice application"

Ptrsan am

"I like it so much very best application"

roman gii

"My best application👍"

Sio Jennifer

"nice so much 👍"

Edward Jones gii

"This application is very useful and very amazing🌴"

Enola RMP

"Very nice and very good app🌴"

Shah g pk By Ryk

"very nice very good app🌴"

Davad wase Sm

Get the App Today

Available for Android 8.0 and above